|

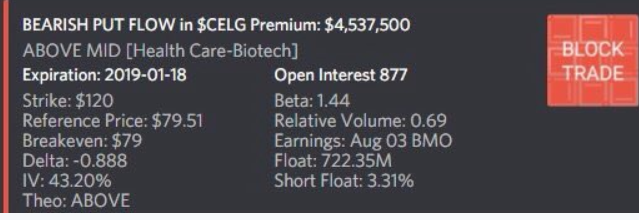

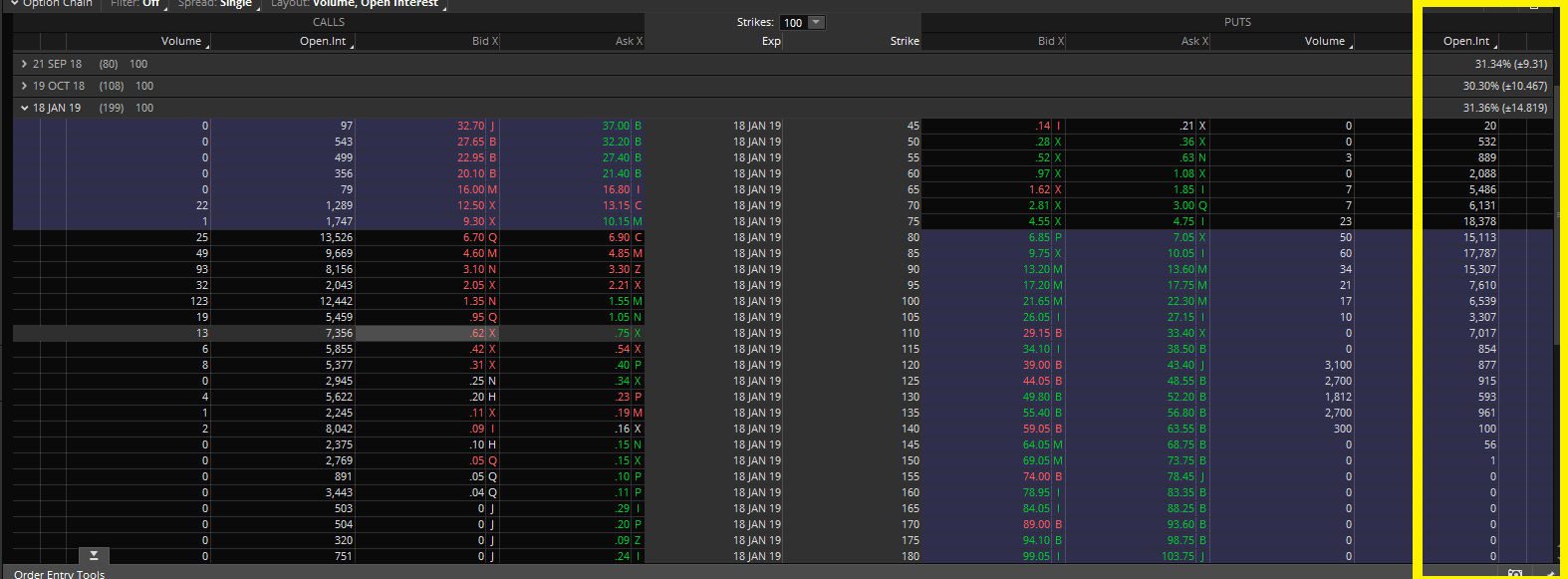

Being long Celgene, I noticed an alert that as an option trader gave me pause:  It struck me as strange. If this was truly bearish, anyone with that kind of money would trust an option trader to buy out-of-the-money to take advantage of convex gamma. This trade was not only in-the-money, it was deep in the money. It is almost -89 delta! So I decided to look at time and sales and found that this is not the only transaction like this. There were plenty. Some were even labelled “spreads”.  A few things jumped out. The first is that even though the price was closer to the “ask” than the “bid”, when you add the “underlying” and the cost of the option, it adds to near the strike. So these could have been bought or sold at very small premium. So I checked the open interest to see how prevalent this has been.  The answer is, very prevalent. That is an unusual amount of open interest for a selection of put strikes that are in the money.

Who could be involved in those transactions? Since I’m long CELG, I remembered that on May 24th, Celgene announced an accelerated $2B buyback program through Citi Bank that will expire on August 31st. I looked at Celgene’s cash flow statement, and as of the end of last year, they had $843M in positive cash flow. Not bad, but where are they getting $2B? Even if they got more cash flow despite a stock that has been struggling for the past year, that would put them in a difficult spot from a cash standpoint. Moody’s even claimed that this repurchase program is a negative for Celgene’s credit. By now you might have put together my theory: Celgene or Citi are selling these puts to finance the accelerated buyback. If this is true, it is brilliant. They sell these puts and collect millions of dollars. The transactions today alone resulted in ~$50.5M of premium collected if this thesis is true. If you took half of the open interest (assuming all the contracts were bought and sold to open), you are looking at ~$500M collected already, or 25% of the total accelerated buyback. Once collected (which might take a little while), I presume that Celgene and Citi would do a measured purchase of the stock. With this power behind it, you can assume Celgene stock will go up, which will lower the value of those puts. When the buyback is completed, Celgene and Citi will buy back those puts at a lower cost. The result? Celgene has their repurchased shares with the money provided to them by the buyers of those puts, likely automated market makers. I do not know if this is legal. It likely is, as the buyers of those puts are responsible for doing their due diligence. It isn’t like Celgene didn’t announce the buyback. If it is legal, it is a clever arbitrage.

0 Comments

Leave a Reply. |

The WizardJason DeLorenzo Archives

September 2023

Categories |

RSS Feed

RSS Feed